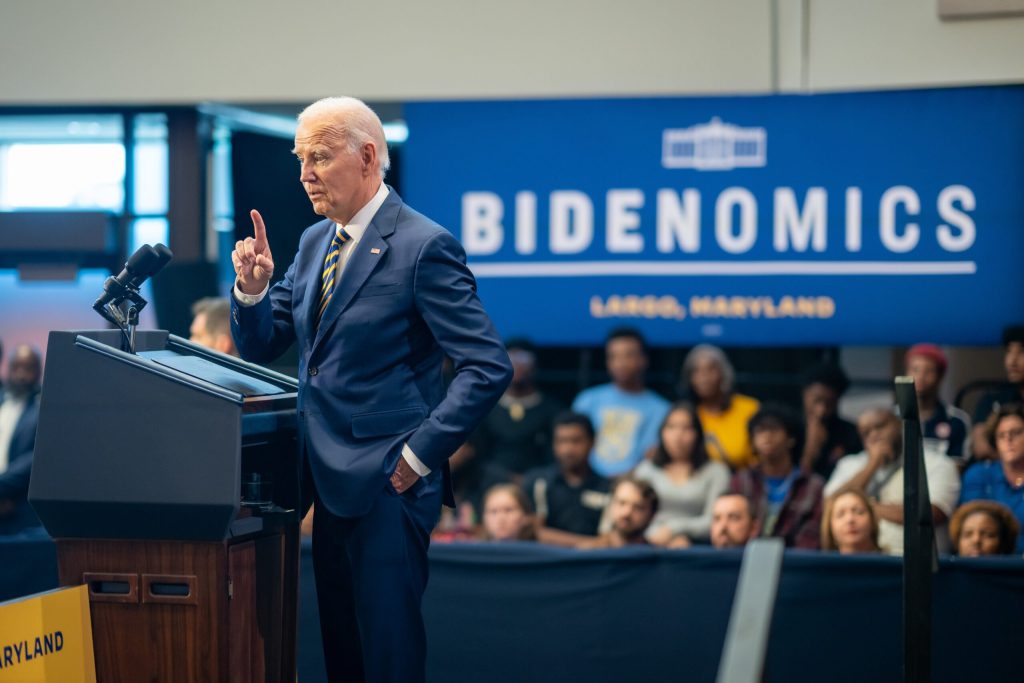

President Joe Biden delivers a speech on the U.S. economy and “Bidenomics”, Thursday, September 14, 2023, at Prince George’s Community College in Largo, Maryland.

(Official White House Photo by Adam Schultz)

Biden talks up the economy’s strong growth but doesn’t address the fact that the inflation rate he’s given us surpasses the GDP growth rate. He also doesn’t mention that much of this growth was funded directly by government stimulus and other financial aid given to the public.

The White House claims the economy is roaring, and mainstream media suggests only Republicans doubt it. However, consumer sentiment is declining, albeit with a slight recent uptick, which both the White House and mainstream media quickly seized upon as a positive trend. Inflation also rose this month, but the White House contends it’s down compared to 2022 levels. It appears the White House chooses to cite macro or micro data depending on what makes them look better.

The average gas price increased by 7% this month compared to last month. However, it remains lower than the $4.90 it hit in 2022. So, I suppose the White House can chalk up another win.

The reality is, both the average American and business owner perceive the economy as dismal and lack confidence in the future. Despite high inflation, the specter of recession still looms large, suggesting stagflation may become a reality in the near future. We could easily find ourselves grappling with growing unemployment alongside escalating prices. Technically, we’ve been in a recession for some time now, but Janet Yellen’s assertion that a recession isn’t defined by two consecutive quarters of negative growth was surprising to me and most university economics professors, as it contradicts the textbook definition of a recession.

Regarding stagflation, it’s defined by rising prices and growing unemployment. In the strictest sense, the White House is correct that we haven’t reached that point yet. More jobs are being created each month. However, if you’re looking for a job, the difficulty in finding one is obvious. This is largely due to the fact that 70% of the new jobs being created are part-time, while about 20% are government jobs. Depending on one’s definition of “jobs,” an argument could be made that significant numbers of new full-time private sector jobs are not being created.

The truth is, the economy has been on shaky ground throughout Biden’s entire administration. The only thing preventing a complete collapse is government stimulus and government job expansion, both of which add to the deficit and debt, merely postponing the inevitable. And that inevitable end is fast approaching.

Several US municipalities have implemented excessively high minimum wages, reaching up to $20 an hour. As a result, retailers, fast food chains, and ride-hailing apps like Lyft and Uber are exiting these markets. Grocery stores are transitioning to self-checkout systems, while fast-food establishments are introducing order kiosks. Moreover, many CVS and Walgreens drugstores have significantly reduced their floor staff, in some instances to just one employee.

Under Bidenomics, we’ve witnessed a 46% increase in gas prices, with mortgage rates inching closer to 7%. Meanwhile, the demand for new mortgages is dwindling.

Real wages, adjusted for inflation, have dropped by an average of $371. The White House’s deception on this matter lies in presenting a chart of inflation that peaked in June 2022 and has since been declining, while wages have been on the rise. At first glance, it may seem that the worst of inflation is behind us and wages now surpass inflation. However, it’s crucial to remember that prices have not decreased.

The rate at which wages are increasing, at 5%, now exceeds the rate of price increases, at 3.2%. However, over the past four years, we’ve seen cumulative inflation of nearly 20%. So, whereas you once earned a dollar, you now earn $1.05, while goods that previously cost $1.00 now cost $1.20. As a result, your real wages, adjusted for inflation, have decreased.

In short, the money you earn buys you less stuff.

Due to a decline in inflation-adjusted income, US savings rates have dropped to 3.6% from the pre-pandemic level of 6%. Credit card delinquencies and car loan defaults have reached record highs. Many Americans report borrowing money each month just to cover their cost of living.

Bidenomics is a disaster, and the White House is still considering cutting interest rates, which would cause inflation to skyrocket.

The post Credit Card Defaults, Inflation, Part-Time Jobs: The Economy Is a Disaster appeared first on The Gateway Pundit.